De-risking too: The world's efforts to de-dollarise

Despite all the talk of de-dollarisation and some movement towards it, the US dollar remains the dominant global currency for now, and it will be an uphill task to shift away from it. Lianhe Zaobao correspondent Lai Oi Lai speaks to academics and financial experts to find out more about the world's pursuit of de-dollarisation as a way of risk management.

The question of who can challenge US dollar dominance has recently become a hot topic in the international community. De-dollarisation may seem out of reach, but following US sanctions on Russia, many countries are already taking unified action in that direction.

"The US sanctions on Russia have made many countries anxious. The harsh reality is that if one day a country that holds a lot of US dollar reserves offends the US, it could freeze those assets," said Pei Sai Fan, adjunct professor at the National University of Singapore (NUS) and Lee Kong Chian School of Business, Singapore Management University, in an interview with Zaobao.

In February last year, the war in Ukraine broke out, and the US announced a ban on US dollar transactions with the Central Bank of Russia, as well as a comprehensive blockade of Russia's sovereign wealth fund, the Russian Direct Investment Fund. Russia was prevented from accessing these funds for emergencies, and could no longer use its reserves to cushion the sharp decline of the ruble.

More countries may settle trade in RMB

Over a year into the war in Ukraine, US Treasury Secretary Janet Yellen recently said in an interview with CNN, "There is a risk when we use financial sanctions that are linked to the role of the dollar that over time it could undermine the hegemony of the dollar."

Yellen pointed out that while sanctions are an "extremely important" tool, it has also prompted some countries to start looking for alternatives to the US dollar.

In January this year, Saudi Arabia's Finance Minister Mohammed bin Abdullah Al-Jadaan said that he was open to using currencies other than the US dollar for trade settlement.

In March, China's state-owned enterprise CNOOC and France's TotalEnergies completed the first liquefied natural gas transaction settled in the RMB. In the same month, China and Brazil reached an agreement to settle trade in their respective currencies. China is Brazil's largest trading partner, with bilateral trade reaching US$150.5 billion last year.

Then in April, Argentina announced that it would start paying for Chinese imports in RMB instead of US dollars, primarily due to the depreciation of the Argentine peso and the continued decline of its US dollar reserves.

"More and more economies will want to settle trade in RMB, because China's role as a bilateral trading partner is becoming increasingly important..." - Cedric Chehab, head of Global Country Risk Research at BMI, Fitch Solutions

P.S. Srinivas, visiting research professor with the Institute of East Asian Studies at NUS, said that since Russia's invasion of Ukraine, the US and other Western countries have imposed sanctions on Russia, prompting some countries to consider how they can strengthen trade using their own currencies or currencies other than the US dollar or euro.

"Countries that currently have agreements with China to settle trade in RMB or local currencies may continue to expand their cooperation with China. It is also possible that more countries will follow suit and seek to settle trade in RMB."

Cedric Chehab, head of Global Country Risk Research at BMI, a research unit of Fitch Solutions, said, "More and more economies will want to settle trade in RMB, because China's role as a bilateral trading partner is becoming increasingly important, and the Chinese government also hopes to further promote the internationalisation of the RMB."

Will the US dollar topple like the British pound?

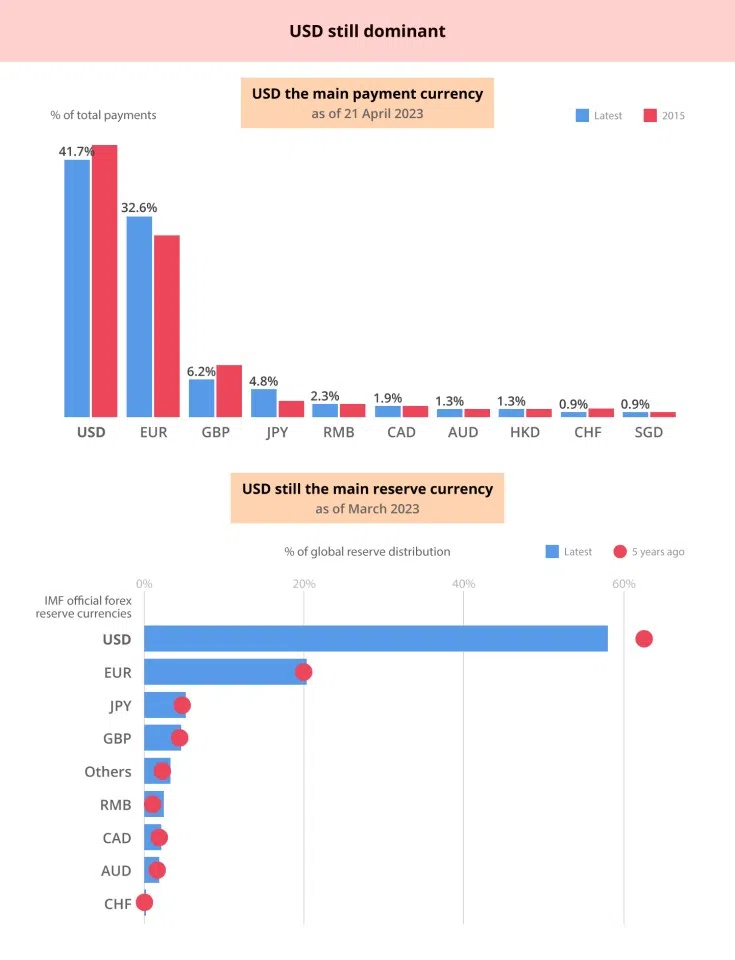

Chehab noted that the US dollar still dominates global trade for now. For example, in the Americas, the US dollar accounts for as much as 96% of export invoices. In other parts of the world - excluding the eurozone where euro transactions are predominant - the US dollar is used in approximately 74% to 79% of transactions.

Although the share of the US dollar as a global reserve currency has decreased from around 71% in the early 2000s to approximately 60% currently, Chehab said that a significant portion of this decrease is driven by an increase in the shares of the euro and the pound. "This has little to do with the rise of emerging market reserve currencies such as the RMB, which only accounts for 2.4% of global reserves," he said.

Nevertheless, some academics still believe that the role of currencies in trade settlement should not be underestimated.

A study published in 2021 by Harvard economists Gita Gopinath and Jeremy Stein highlights the fundamental connection between the US dollar as the primary currency for invoicing by non-US exporters and its prominent position in the global banking and financial industry.

According to Gopinath, former chief economist at the International Monetary Fund, and Stein, a former member of the US Federal Reserve, the large volume of US dollar invoices in international trade creates an increased demand for US dollar deposits, giving the US dollar a disproportionate advantage in reducing borrowing costs. Hence, non-US exporters are more willing to invoice in US dollars in order to obtain these cheap US dollar funds.

The interaction between these factors further solidifies the US dollar's position as a global currency. However, Gopinath and Stein argue that in a changing world landscape, this could be a double-edged sword for the US dollar.

They said, "Even in the face of rapid global export growth in other economies such as Europe and China, the US dollar can still maintain its dominant position in the medium term." However, they added that in the long run, "if the gap between the US and these economies widens to a certain extent, the US dollar could fall from the world stage, as what happened with the British pound in the early 20th century."

Before the First World War, the British pound was the major global currency, with over 60% of global trade invoiced, financed and settled in pounds. In 1944, to address the chaotic state of the international monetary system at the time, representatives from 44 countries convened in the US and formally established the Bretton Woods system, centred around the US dollar.

A multipolar economic and trade system with three major currencies

On whether the US dollar will follow the path of the British pound, Srinivas believes that the situation is different today, as compared with when the US dollar displaced the pound as the world's major currency.

"In the long run, it is possible for countries to use multiple major currencies in trade. China is the world's second largest economy, and the RMB could become a major currency alongside the US dollar and others," Srinivas said.

However, it is unlikely that the RMB will be on par with the US dollar and become a major global currency in the short term. Srinivas said, "Even in the long run, the Chinese government would need to take more policy actions to make it possible."

Srinivas noted that the US dollar is the preferred global currency primarily due to the sustained strong demand for the dollar outside the US, including from the eurozone. "For the RMB to seriously challenge the US dollar, it would need to reach a similar level of demand," he remarked.

"Looking ahead, I believe that three major groups will gradually take shape: the US dollar group, the euro group and the RMB group. This will evolve into a multipolar world in terms of politics, economics and finance." - Cedric Chehab

He added that there are still obstacles to the quicker internationalisation of the RMB. China's capital controls, underdeveloped financial markets, limited confidence among foreigners in the unrestricted access to RMB assets, and concerns about government intervention in the currency and financial markets are all reasons that impede further rapid internationalisation of the RMB.

As for whether the euro can challenge the dominance of the US dollar, Chehab believes that the eurozone economies face significant challenges in terms of fiscal burdens, the efficiency of the currency union, and demographic structures.

"Looking ahead, I believe that three major groups will gradually take shape: the US dollar group, the euro group and the RMB group. This will evolve into a multipolar world in terms of politics, economics and finance," he noted.

US dollar to dominate for at least another decade

In a research report on de-dollarisation, UOB's Global Economics and Markets Research executive director Suan Teck Kin, economist Ho Woei Chen, and senior FX strategist Peter Chia noted, "When Europe's single currency, the EUR, was launched in Jan 1999, it was widely regarded as a challenger to the USD's dominance. More than two decades later, the single currency had made some inroads (accounting for 33% share of SWIFT payments and just about 1/5 of international reserves) but did not gain much adoption outside of Europe."

Suan et al. believe that with the US dollar's robust global financial infrastructure and interconnectedness, such as the SWIFT network that supports the global financial system, the currency will continue to maintain its dominant position for at least the next decade, and possibly even longer.

SWIFT has over 11,000 financial institution members; in 2021, it processed a daily average of 42 million payment and securities transactions.

Russia faced international sanctions after it annexed Crimea in 2014, prompting the development of its national electronic payment system Mir and financial information transmission system SPFS. Following the outbreak of the war in Ukraine, most Russian banks were removed from the SWIFT network, and international credit card companies such as Visa and MasterCard suspended operations in Russia, leading to a surge in demand for Mir, with 182.3 million cards issued last year, up by 60%.

Mir can only be used within Russia and some countries friendly to Russia, while the SPFS has only over 400 members. Nonetheless, this highlights the efforts of some countries to bypass existing channels and reduce dependence on the US dollar system.

Building a digital Asian currency initiated and operated by the community is the only way to achieve true de-dollarisation... - Pei Sai Fan, adjunct professor, NUS and SMU

Can digital currencies accelerate de-dollarisation?

Whether it is the US dollar, euro or RMB, Professor Pei believes that the matter still revolves around sovereign currencies. He said, "Many people talk about de-dollarisation and not being constrained by the dominance of the US dollar, but aren't other currencies also sovereign currencies of third-party countries? How can we ensure that they won't become another hegemony?"

Pei previously proposed a similar idea to what was Facebook's Libra - using blockchain to build a digital Asian currency that would not be the legal tender of any country within the region, nor a common legal tender of any regional organisation or unified market like the euro.

Pei said that building a digital Asian currency initiated and operated by the community is the only way to achieve true de-dollarisation, and he believes that the Asian Infrastructure Investment Bank or the Asian Development Bank are the most suitable institutions to initiate this.

"This requires careful consideration, patience, and the efforts and consensus of multiple parties, which is not easy," he remarked.

Looking at the current situation, Pei believes that central bank digital currencies (CBDCs) could potentially impact the US dollar as an international trading currency, especially in the case of multiple central bank digital currencies (mCBDCs).

Pei noted that the aim is not for mCBDCs to create a new currency, but rather using digital currencies issued by various countries to develop a common platform based on blockchain technology, so that any two countries can trade without the need for a third-party sovereign currency.

In the second half of last year, the Bank for International Settlements and the central banks of Hong Kong, mainland China, the United Arab Emirates and Thailand conducted tests on international trade transactions using a common mCBDC platform.

Representatives from 20 commercial banks from these four economies conducted over 160 payments and settlements totalling US$22 million in Payment versus Payment (PvP) foreign exchange transactions. Within five weeks, the four central banks issued over US$12 million in CBDCs.

However, Pei emphasised that CBDCs will not have a significant impact on the status of the US dollar as a reserve and safe-haven currency.

Companies should be familiar with and prepared to use more currencies alternative to the US dollar in their business operations as an important component of risk management and their hedging strategies.

BMI's Chehab does not rule out the possibility of CBDCs becoming an important alternative to major currencies such as the US dollar, but he remains sceptical. "The value of CBDCs may still be linked to the economic fate of a specific economy and priced in that economy's currency, which means that major currencies such as the US dollar will continue to maintain their dominant position," he said

There is still a long way to go to de-dollarisation. Suan et al. believe that the financial sanctions on Russia have given companies a warning that, under extreme circumstances, they may be forced to change their business practices overnight. Companies should be familiar with and prepared to use more currencies alternative to the US dollar in their business operations as an important component of risk management and their hedging strategies.

This article was first published in Lianhe Zaobao as "去美元化 知易行难".

Related: Will de-dollarisation help China and Russia shape a new world order? | Quit the dollar: Can Asia build its own digital currency and digital payment infrastructure? | The impact of the Russia-Ukraine war on the Chinese economy | China's efforts to internationalise RMB gaining a foothold in SEA