China lines up yet more aid for the property sector, but will it be enough?

(By Caixin journalists Chen Bo, Wu Xiaomeng, Huo Kan, Wang Juanjuan, Niu Mujiangqu, Liu Ran, Zhang Yuzhe and Han Wei)

China is poised to roll out more policies to assist developers in an increasingly desperate attempt to arrest a protracted downturn of the multi-trillion-dollar property sector, a key pillar of the world's second largest economy, Caixin has learned from sources close to policymakers.

However, reversing the downturn, that has seen housing sales plunge 28.4% in the first ten months of this year, will not be easy, and depending solely on financial tools may not be enough as the industry undergoes fundamental change, analysts said.

Supportive measures underway

Any substantial recovery will also rely on the restoration of consumer confidence and the revival of the overall economy, which slowed to 3.9% in the first three quarters, well below the 8.1% for all of last year and the government-set target of around 5.5% for 2022, they said.

Since mid-November, a wave of supportive measures has been unveiled to prop up the property market that has been mired in a record slowdown and deepening liquidity crunch for over a year.

These have included a government-backed bond issuance programme, relending quotas to support unfinished projects and easing restrictions on developers' access to pre-sale funds. The measures are set to inject hundreds of billions of RMB in new funding into the property sector.

The policies, which are designed to stimulate demand, improve developers' financial predicament and restore market confidence, is seen as "the most crucial pivot" away from the previous stance of tightening regulation over the real estate sector...

The most recent support package was unveiled on 11 November, when the People's Bank of China and the China Banking and Insurance Regulatory Commission issued a 16-point plan that included an expansive range of measures to encourage financial institutions to beef up their support of homebuyers and developers.

The policies, which are designed to stimulate demand, improve developers' financial predicament and restore market confidence, is seen as "the most crucial pivot" away from the previous stance of tightening regulation over the real estate sector, economists have said.

Shares of Chinese developers surged following this announcement on investor expectations that Beijing was planning to reverse most of its financial tightening measures.

The Hang Seng Mainland Properties Index that tracks Chinese developers jumped almost 20% in the two days following the 16-point announcement. The Hong Kong-listed shares of Country Garden Holdings Co. Ltd., China's largest developer by sales value, jumped 45.5% the following trading day, while Longfor Group Holdings Ltd. climbed 16.5%.

More measures are in the works for the government's rescue package for the property industry and will be put in place in the near future, Caixin learned from sources close to policymakers. Much care will be taken to ensure the policies are implemented properly, said the sources, who did not specify what they might be.

Perfect storm

Since China's commercial housing market was opened to private investment in 1998, the rise of the property sector has been unstoppable, despite numerous rounds of government controls to rein in speculation and soaring prices. In nearly three decades, average housing prices in 100 cities have grown by roughly sevenfold, according to data from the National Bureau of Statistics.

Down through the decades, roughly every three years the government would step in with policy tools in an attempt to temper the rise. But after each round of new measures there would only be a small retreat in prices, followed by a rebound that would take them higher again, as people bet on the continued growth of the economy and housing market.

But that has changed over the past two years. China's shifting demographic structure that has seen its ageing population grow at a faster pace than most other countries combined with a birth rate plunging to lows not seen since the 1960s, as well as increasing urbanisation and slowing economic growth means the housing market is undergoing profound change.

Over recent decades, China's developers had mainly relied on quick turnover and high leverage to fuel their business expansion.

Disruptions due to the Covid-19 pandemic and consequent strict control measures such as snap lockdowns have only added more stress.

China's demand for new housing reached a turning point once the urbanisation rate reached 63.9% in nominal terms, said Huang Qifan, former Chongqing mayor, in a public speech in January. That milestone was reached in 2020, according to data platform Statista.

In that year, China's per capita housing construction area was 41.76 square metres, and the national vacant housing ratio was about 20%, relatively high for a country with a fast-growing housing market, according to Huang.

Over recent decades, China's developers had mainly relied on quick turnover and high leverage to fuel their business expansion.

The four largest Chinese developers - China Evergrande, Country Garden, China Vanke and Sunac China - have an average debt-to-asset ratio of over 80%, much higher than their counterparts in Japan, the US and Hong Kong, according to a July study by Zhou Qiong, a senior analyst at Shanghai Institute for Finance and Development.

Double-edged sword

This highly leveraged growth model proved to be a double-edge sword for Chinese developers, on the one hand fueling their rapid growth, but on the other creating huge risks, said Zhou.

To rein in the excessive leverage, regulators in 2020 introduced the "three red lines" policy, which set out a trifecta of financial metrics to control the amount of debt developers could take on.

These were: a liability-to-asset ratio (excluding presales) of no more than 70%; a net debt-to-equity ratio of under 100%; and cash holdings at least equal to short-term debt.

A further "two red lines" - which set specific limits on the proportion of banks' lending to developers and mortgage loans as part of their total lending based on the lenders size and asset quality - were implemented in January 2021.

The policies were a game changer and hit the brakes on the housing market, which had been struggling since 2020 with weakening demand and Beijing's campaign of deleveraging, that began in 2017 and returned last year after a pause due to the outbreak of Covid-19, which itself further dampened people's confidence.

About 40% of China's private developers had already defaulted on some bonds, with another 30% in imminent danger of following suit. - Zhu Haibin, Chief China Economist, JPMorgan Chase & Co.

The deleveraging campaign meant that developers must maintain stable liquidity by increasing sales and expanding their profit margins, according to one real estate company source. But in reality, companies were squeezed by rising development costs and slowing sales, as well as fewer alternative funding sources, said the person.

By the second half of 2021, it had become a perfect storm. Amid growing headwinds from the market and policy measures, China's housing sales have been dropping at a double-digit pace every month since August 2021.

In the ten months from January through October this year, national home sales dropped 25.6% in terms of square metres and 28.2% in terms of value, according to the statistics bureau.

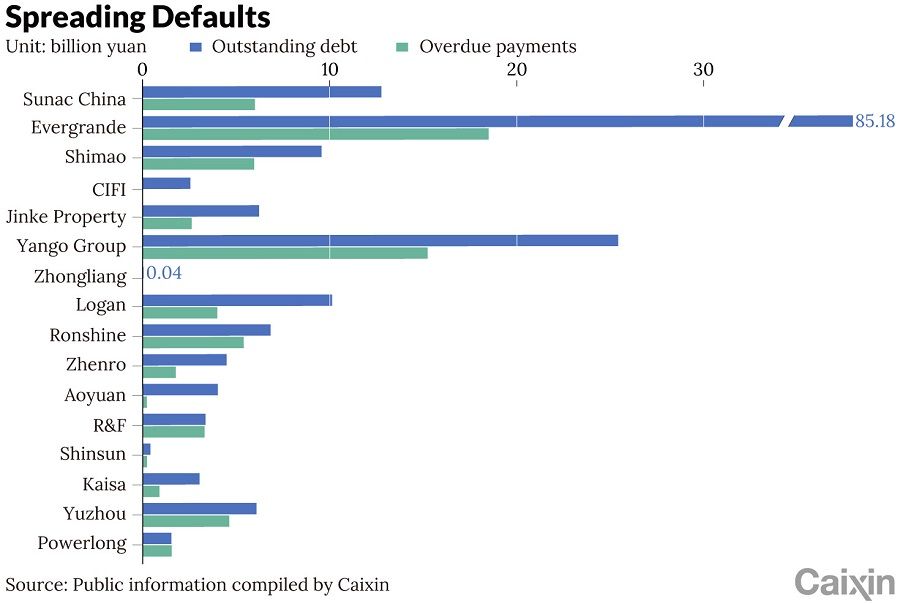

Slowing sales further squeezed developers struggling with tightened financing rules. The crisis at China Evergrande, the most indebted developer whose interest-bearing liabilities ballooned to around 717 billion RMB (US$110 billion) at the end of 2020, ignited market fears and triggered an avalanche of bond defaults.

Private developers, accounting for 70% of the country's property market, were hit the hardest. About 40% of China's private developers had already defaulted on some bonds, with another 30% in imminent danger of following suit, said Zhu Haibin, chief China economist at JPMorgan Chase & Co., last week.

In acknowledgement of the crisis, regulators have softened their tone over the compliance of the "three red lines" policy, Caixin has learned. They have also decided to give banks more time to comply with the "two red lines" that limited the size of their lending for property development and mortgage loans.

Rigid application of requirements will exacerbate the liquidity crisis, a regulatory official told Caixin. The change reflects regulators taking the prevailing industry and economic environment into consideration as it tweaks the deleveraging campaign.

Contagion spreads

The contagion has now spread to other industries, with analysts saying that more than 40 sectors in the real estate industry chain, including construction, building materials, home appliances and furniture, have begun to feel the pinch.

Publicly available market data showed that a total of 336 construction companies have declared bankruptcy or undergone reorganisation over the past few months, including some industry leaders. Although they account for only a small portion of China's some 120,00 registered construction firms, the figure is still significantly higher than previous years.

Building materials companies recorded a 32% drop in net profits in the first three quarters of this year, on top of an 8.8% decline in revenue, according to a report from BOC International Holdings Ltd.

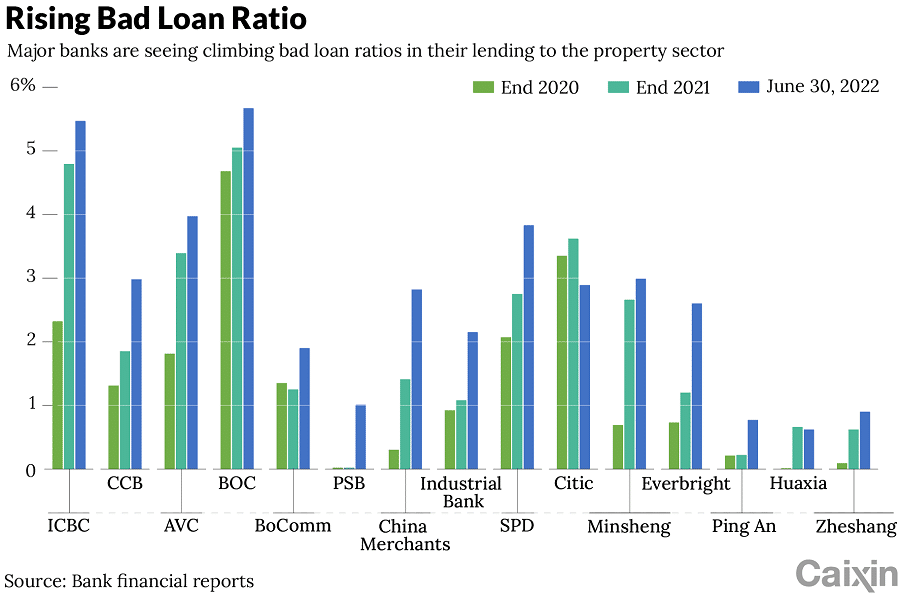

Unsurprisingly, unease has also grown in the banking sector, which has lent trillions of RMB to developers and had counted 39 trillion RMB of mortgage loans - about 75% of their total property-related lending by the end of September - as its most stable assets with bad loan ratios long holding below 0.5%.

... there is still room for China's property market to return to growth as potential demand from people seeking to improve their standard of living remains unchanged.

And although property development loans account for less than 10% of entire lending by all of China's banks, a real estate market crisis will still threaten the banking sector, a bank risk control manager said.

"Housing is a credit instrument with strong financial attributes. It is key collateral in financial credit and involves various institutions such as banks, trusts, and asset managers," said the risk controller. "If there is a problem in the real estate industry, the operation of the entire financial system will be affected."

The housing market downturn has also put pressure on local government coffers as land sales have slowed and individual families are also being hurt by shrinking property values. Earlier this year, stalled construction by cash-strapped developers triggered massive mortgage strikes by worried homebuyers in dozens of Chinese cities.

'Epic crisis'

The logical order of China's real estate industry has been rewritten and superimposed with cyclical issues from within the industry and the whole economy, according to an industry insider. Allowing individual risks in the industry to accumulate will trigger an "epic crisis," said the person.

However, there is still room for China's property market to return to growth as potential demand from people seeking to improve their standard of living remains unchanged, analysts said.

China's per capita living area is less than 29 square metres, smaller than the upper limit of international standards of 50 square metres. Meanwhile, the country still has hundreds of millions of low-income people, who rely on subsidised housing to improve their living standards.

To maintain the health of the industry while ensuring that people's demands are met will require long-term systemic planning to set up mechanisms to ensure reasonable land supplies and an effective taxation system to curb speculation, analysts said. These will require joint efforts between numerous government departments, they said.

Economist Ren Zeping, who was formerly chief economist at struggling real estate giant China Evergrande and is now an online influencer, agrees, saying in a recent article that China should push forward city cluster development, reform the land supply system, launch a pilot property tax and expand rental housing to address long-term challenges in the property sector.

But the question, remains: Will that be enough?

Wang Liwei, Peng Qinqin and Xia Yining contributed to the story.

Read part two and part three of the story here and here.

This article was first published by Caixin Global as "Cover Story: China Lines Up Yet More Aid for the Property Sector, But Will It Be Enough? (Part 1)". Caixin Global is one of the most respected sources for macroeconomic, financial and business news and information about China.

Related: Can SOEs' property buying spree save China's ailing property market? | Can China save its property market and economy amid fastest-spreading outbreak to date? | Export slowdown reveals cracks in one of China's economic pillars | Has China's monetary policy reached its limit? | Bartering garlic for homes: China's uphill fight to revive the real estate market