China's economy is bound to recover in 2023

China research analyst Chen Long gives a positive assessment of China's economic prospects in 2023, pointing out that the swift U-turn on Covid policies may wreak havoc in the short-term, but be the catalyst to drive economic growth in the Year of the Rabbit. Variables are looking favourable, with the consumer spending and housing sector showing potential, and government policies going in the right direction.

China's economy is bound to recover in 2023 after the slump in 2022, and the recovery will likely be better than expected. The consensus for GDP growth seems to be around just 5%, and "a bumpy road to normal" is often mentioned for post-zero-Covid China.

But maybe the road to normal is not that bumpy. China's Covid policy U-turn in November and December has led to the rapid spread of Covid infections, which caused medicine shortages and overflowing hospitals. The central government estimated that almost 37 million people across the country got Covid in one day in late December. Local authorities in some of China's most populous provinces have estimated that nearly 90% of their residents have already gotten Covid and recovered by mid-January.

The fact that China seems to have reached the peak of this massive Covid wave in late 2022 is good news for 2023. It is partly because the base effect favours year-on-year growth in 2023 even more.

Worst is over?

The fact that China seems to have reached the peak of this massive Covid wave in late 2022 is good news for 2023. It is partly because the base effect favours year-on-year growth in 2023 even more. It is also partly because the recovery is taking place earlier and faster than expected. Anecdotal evidence in major cities as well as subway traffic data suggest that the rebound has been very rapid. Some popular tourist destinations are receiving customers at close to 2019 levels.

Domestic demand will be key this year, especially in terms of real estate, and consumption, which were the two biggest laggards in 2022.

Chinese household consumption fell 0.2% in 2022 from 2021, and new home sales were down about 27% year on year. The repeated lockdowns were a key reason for their poor performance. Now that China is transitioning to living with Covid, lockdowns will no longer be an issue, which removes a major roadblock for people to consume and purchase housing.

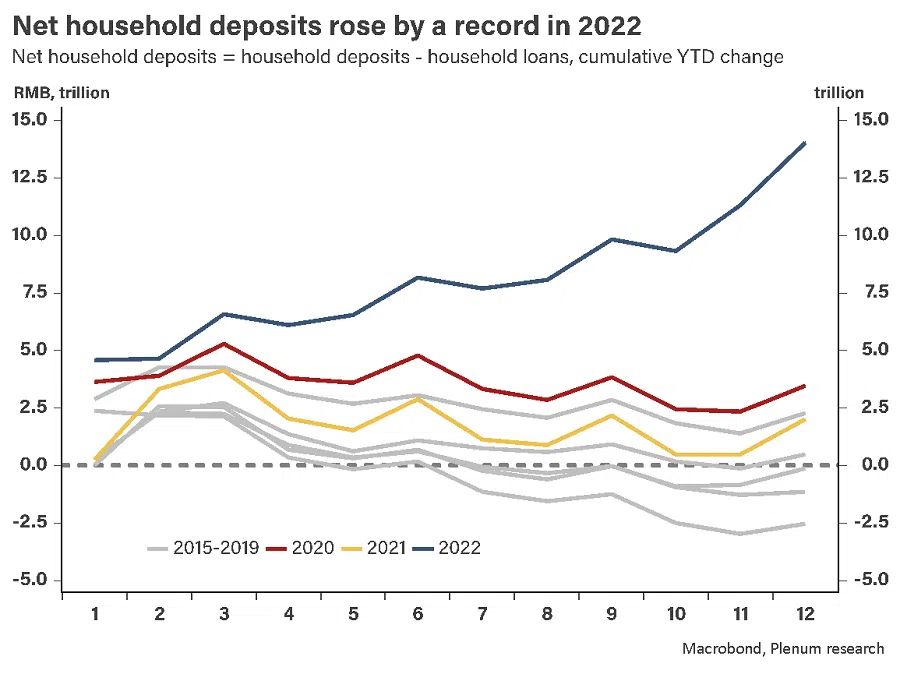

From saving to spending

Chinese households have the spending power, too. They have saved a lot more in 2022 than in previous years. In 2022, Chinese household deposits rose by over RMB 17 trillion, an all-time high, while their loans only rose by RMB 3.7 trillion, about half of previous years. Net deposits rose by RMB 11 trillion, five times the increase in 2020, which was the previous record.

Although Beijing is unlikely to launch a nationwide campaign to hand out cash to households due to inflation fears, Chinese households are able to spend and borrow more with much less leveraged balance sheets, as long as they are not facing any restrictions. In the past three years, retail sales were highly (reversely) correlated with lockdowns. There is a reason to believe that retail sales will see a boost in 2023, barring another huge Covid wave.

The latest survey by the central bank in Q4 2022 shows that 61.8% of households want to save more, a record high. Meanwhile, the share of households willing to consume more declined to 22.8%.

Yet, confidence could still be a problem. The latest survey by the central bank in Q4 2022 shows that 61.8% of households want to save more, a record high. Meanwhile, the share of households willing to consume more declined to 22.8%. We believe this pattern may be reversed after people get used to living with Covid, although what the reversal will look like is uncertain.

For the real estate market, new home sales in 2022 declined to 1.15 billion square metres. This was a much-needed correction from a structural perspective because the 1.5 billion square metres in annual sales in 2019-21 far outstripped people's housing needs. A lot of that was probably speculative and over drafting future demand.

... we think an upside surprise, such as a year-on-year sales increase of less than 10%, is more likely than a downside surprise.

Optimism in housing sector and government policies

1.15 billion square metres is close to our base-case estimate for the average annual new home demand in this decade. More contraction is still expected to take place later this decade but is no longer urgent. With extremely accommodative policies and very low expectations (most expect a low single-digit decline), we think an upside surprise, such as a year-on-year sales increase of less than 10%, is more likely than a downside surprise. Cities with more population inflow, low housing inventory, and faster recoveries could lead the market turnaround, and sentiments could change fast.

The politics are favourable too. The new premier is all but certain to be Li Qiang, who became the Communist Party's number two after the 20th Party Congress. He had worked with President Xi in Zhejiang province 20 years ago and is believed to be a close ally. He and the new State Council have strong incentives to deliver better economic growth in their first year. They are well aware that 2022 had left businesses and investors traumatised, and thus probably want to boost the economy as fast as possible.

Beijing has already made efforts to deliver more policy support, not waiting until the new government is officially formed in March. The Central Economic Work Conference, China's most important annual meeting for economic policy in December, struck a very pro-growth tone. It reiterated the "unswerving" support for the private sector, as well as vowed to help the internet platform companies lead development.

The sweet talk has been backed by real actions. The central bank recently said that the rectification campaigns at Ant Group are close to the end, and China's ride-hailing giant Didi Chuxing is able to allow new user registration again after 18 months of suspension. More policy tailwinds can be expected.

The threat of supply chain relocation away from China has not materialised much but could be a lasting concern.

Headwinds

External demand was the biggest driver for China's growth in the past two years, but it will likely become a headwind this year. Export growth has already fallen to the negative territory since October, and the country may face a year-on-year decline in goods exports in 2023, after six consecutive years of increase, as demand from the US and Europe softens. The threat of supply chain relocation away from China has not materialised much but could be a lasting concern.

Another long term concern is demography. In 2022, China saw its first population decline in more than 60 years. New births fell to 9.6 million, down from 10.6 million in 2021, while deaths increased to 10.4 million. The head of the statistics bureau bluntly admitted that this trend cannot be reversed in the next ten to 15 years, which will adversely impact the economy, particularly in terms of housing. Regional disparity, already stark, will only worsen. And areas with large population decline will also suffer shrinking economies.

![Hokkien roots, Brunei soil: My father’s journey across borders and spiritual planes [Eye on Fujian series]](https://cassette.sphdigital.com.sg/image/thinkchina/71f359b221f9d122e33e939974a2a8159629f5990340bdf70135adfea2d6a086)

![[Video] Jereme Leung: From Nanyang to Jiangnan — where taste becomes memory](https://cassette.sphdigital.com.sg/image/thinkchina/915587e6ef38f403df0792bdbbf90b20fc4fb5d39b299feacefd74b9bf8e685d)

![[Big read] Not just nukes: Why the US won’t strike North Korea](https://cassette.sphdigital.com.sg/image/thinkchina/488cd6c44e77de6d201490f20871fd4192f527212893e399fb541da50802c7f8)