China's trillion-dollar local government 'hidden debt' dilemma

As China's financial system remains plagued by trillions of dollars in local governments' hidden debt, policy makers may need to take drastic measures to solve the problem.

(By Caixin journalists Zhang Yukun, Xia Yining and Ding Feng)

China's financial system remains plagued by trillions of dollars in local governments' hidden debt, as they have long turned to off-the-books borrowing to plug funding shortfalls, which have grown significantly due to the pandemic and property crisis.

To solve the problem, policy makers may need to take drastic measures, such as allowing local governments to sell bad debt to asset managers and giving them a bigger slice of tax revenue, financial scholars said.

The scholars gathered to discuss the challenges posed by local government borrowings, especially off-balance-sheet debt, as well as possible solutions, at a seminar hosted by the National School of Development (NSD) of Peking University on 9 September.

Hidden debt

China's local authorities have accumulated trillions of dollars of liabilities off the books. They mainly include bonds issued by local government financing vehicles (LGFVs), state-owned companies set up to finance local investment such as building infrastructure. Debt is also hidden in public-private partnership projects, shady loan contracts, and other channels used by local governments to raise money.

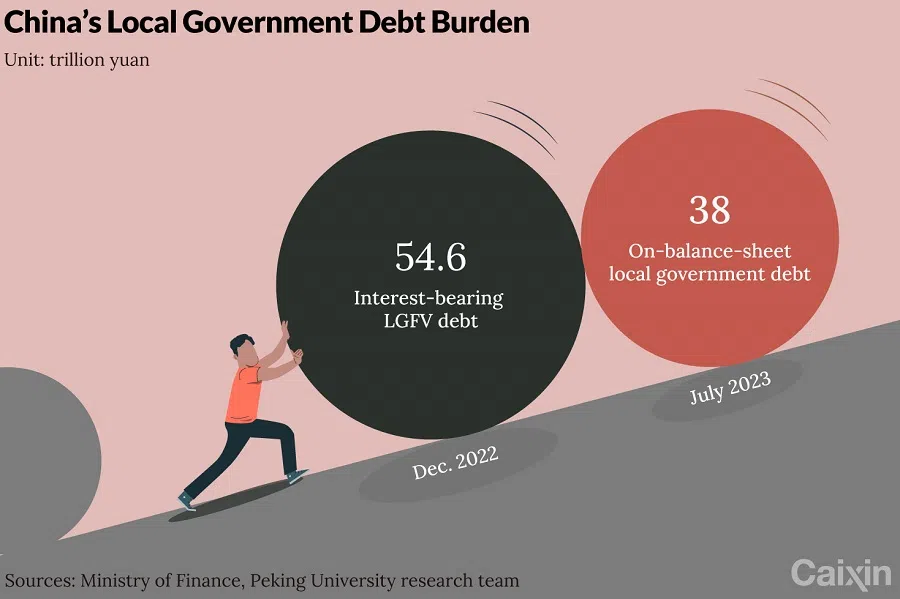

There is no publicly available official data on the current scale of the hidden debt. But research by a team including Hu Jiayin, an assistant professor of finance at the NSD, showed that interest-bearing LGFV debt had ballooned to 54.6 trillion RMB (US$7.8 trillion) as of the end of 2022 from 32.6 trillion RMB four years before, up two-thirds, despite the central government's persistent efforts to resolve it. Local governments are obliged to repay some of the debt, according to the research.

Outstanding local government debt on the books totalled 38 trillion RMB as of the end of July, official data showed.

If both on-the-books debt and all of the interest-bearing LGFV debt were taken into consideration, local governments would have had to spend 19% of their total fiscal revenue - which consists of general public budget revenue and government-managed fund revenue - paying interest to creditors last year, Hu said at the seminar.

Interest payment has become more and more challenging for local governments, especially for economically weaker regions, after plunging land sales and three years of costly Covid-19 controls drained their fiscal income.

The gravity of the problem has sent it to the top of Beijing's political agenda, with the Politburo, the ruling Communist Party's top decision-making body, vowing in July to create and implement "a package of debt-resolving plans".

The details of the package haven't been released. Caixin recently reported that the government may allow a dozen regions under especially heavy debt burdens, including Tianjin municipality and Guizhou province, to issue a combined 1.5 trillion RMB worth of special refinancing bonds to bring hidden debt onto the books.

But bringing hidden debt onto the books won't solve the fundamental issue that most local governments simply don't have the resources to pay back what they owe. - Yao Yang, dean of the National School of Development

It wouldn't be the first government-led debt swap programme aimed at transmuting hidden debt into on-balance-sheet bonds. More than ten trillion RMB of swap bonds were issued in previous debt-refinancing programmes from 2015 to 2022, according to analysts' estimates.

But bringing hidden debt onto the books won't solve the fundamental issue that most local governments simply don't have the resources to pay back what they owe, said Yao Yang, dean of the NSD.

Potential short-term solutions

To resolve existing hidden debt, the central government should carry out another round of audits for local government debt, said Zhang Ming, a deputy director of the Institute of Finance and Banking at the Chinese Academy of Social Sciences. Before the audit, local officials should be informed that this would be the last chance for them to ask for help so that they would be encouraged to report their debt truthfully, he said.

Once the off-the-books debt is laid out clearly, the central government should help localities deal with their hidden debt based on how the proceeds had been used, Zhang added.

If the proceeds had been used to pay for public goods, such as Covid-19 controls, local governments can swap the debt into general bonds; and if their finances don't allow them to do so, the central government can issue bonds to help with the swap, Zhang said. Whereas, if funds had been invested in other types of projects, including those that have failed to generate enough returns to cover repayment, local governments can restructure the debt and then sell stakes in state-owned enterprises (SOEs) to raise money for repayment.

Likewise, Yao suggested that local governments raise money by selling their assets, including cash-generating ones, to bad-debt managers.

Financial institutions should also participate in restructuring local governments' hidden debt, said both Zhang and Yao, because they were responsible for having lent to LGFVs indiscriminately.

... China's tax sharing system means that revenue from some types of taxation, including value-added tax, is split between local and central governments, with the latter redistributing the income mainly to poorer regions.

Reforms for consideration

A major cause for the buildup in hidden debt is that local authorities can't balance how much they have to spend - including paying for public goods and other investments to grow the economy - with how much they earn from tax revenue and other transparent fundraising channels such as land sales.

As the property market has yet to recover from a severe debt crisis, demand for land remains muted.

Meanwhile, China's tax sharing system means that revenue from some types of taxation, including value-added tax, is split between local and central governments, with the latter redistributing the income mainly to poorer regions.

Local governments should be allowed to take a bigger slice of tax revenue, while the central government should shoulder more social welfare expenditure, Zhang said.

But Yao said that local governments would continue raising debt even if their income level matches their spending burden. "As long as a local government longs for (economic) development, it will take on more debt; and this is what happens around the world," he said.

China's finance ministry has said that local authorities don't bear the responsibility of repaying the debt of LGFVs or other SOEs.

To curb hidden debt, Yao's "radical suggestion" is to integrate all local SOEs, including LGFVs, into government budgets to put them under lawmakers' supervision.

China's finance ministry has said that local authorities don't bear the responsibility of repaying the debt of LGFVs or other SOEs. But Yao said local governments should publicly claim responsibility for their hidden debt and that LGFVs should be allowed to go bankrupt, so that "investors won't blindly buy government-backed bonds and banks won't blindly lend to local governments".

Meanwhile, a contingency plan should be in place, said Zhang, so that in the case of large-scale LGFV defaults or broader financial contagion triggered subsequently, different levels of governments will be equipped to respond.

This article was first published by Caixin Global as "In Depth: China's Trillion-Dollar Local Government 'Hidden Debt' Dilemma". Caixin Global is one of the most respected sources for macroeconomic, financial and business news and information about China.

Related: Chinese local governments facing debt crisis: Waiting for bailouts | Clock ticking on Country Garden's debt bomb | Will China's economy suffer a 'lost decade' just like Japan? | China local governments' fiscal stress may roll over to 2023, think tank warns | China's local governments going bankrupt?

![Hokkien roots, Brunei soil: My father’s journey across borders and spiritual planes [Eye on Fujian series]](https://cassette.sphdigital.com.sg/image/thinkchina/71f359b221f9d122e33e939974a2a8159629f5990340bdf70135adfea2d6a086)

![[Video] Jereme Leung: From Nanyang to Jiangnan — where taste becomes memory](https://cassette.sphdigital.com.sg/image/thinkchina/915587e6ef38f403df0792bdbbf90b20fc4fb5d39b299feacefd74b9bf8e685d)

![[Big read] Not just nukes: Why the US won’t strike North Korea](https://cassette.sphdigital.com.sg/image/thinkchina/488cd6c44e77de6d201490f20871fd4192f527212893e399fb541da50802c7f8)